At SignatureFD, we believe giving back can be one of the most meaningful ways to find your Net Worthwhile®. As the end of 2025 approaches, charitable giving may be at the forefront of your year-end planning. This usually begs the question, “How can I make a meaningful impact on the causes I care most about while optimizing my financial plan?”

Below, we have identified three key elements we believe are crucial to successful philanthropic strategies: Donor-Advised Funds (DAFs), Charitable Bunching, and Qualified Charitable Distributions (QCDs). These strategies allow many donors to navigate tax complexities, maximize charitable contributions, and help provide a brighter future for the causes they hold dear.

Before implementing a charitable giving strategy, it is important to review the increased standard deduction thresholds to gift in a tax-efficient manner. Below, we have outlined the 2025 standard deduction rates.

|

Filing Status: |

2025 STANDARD DEDUCTION |

|

SINGLE |

$15,750 |

|

MARRIED (JOINT) |

$31,500 |

|

MARRIED (SEPARATE) |

$15,750 |

|

HEAD OF HOUSEHOLD |

$23,625 |

|

OVER 65 OR BLIND (MARRIED) |

$1,600 |

|

OVER 65 OR BLIND (SINGLE) |

$2,000 |

Donor-Advised Funds (DAFS)

To implement this strategy, gift cash or appreciated assets to a charitable investment account, called a Donor-Advised Fund (DAF). You receive a charitable deduction for that year up to the total amount donated (subject to adjusted gross income (AGI) limitations). Donating appreciated, long-term assets to a DAF can help minimize capital gains taxes while providing an income tax deduction.

DAFs can also be a particularly valuable strategy in high-income years, e.g., when completing Roth conversions, selling a business, exercising a substantial number of non-qualified stock options, or the vesting of a large number of restricted stock units, or realizing significant capital gains from a large transaction. By contributing to a DAF during these years, you may offset the higher taxable income while frontloading future charitable gifts.

At the time of the gift, you do not need to specify which charities you want to support. When you are ready to distribute funds from the DAF, you submit a grant recommendation naming the charity or charities of your choice. SignatureFD partners with several DAF platforms, including DAFgiving360 (formerly Schwab Charitable), Fidelity Charitable, Cobb Community Foundation, Community Foundation for Greater Atlanta, Foundation for the Carolinas, and National Christian Foundation.

DAFs can also serve as an effective tool for implementing a charitable bunching strategy described next. For example, donors who wish to “bunch” several years’ worth of charitable contributions into one tax year can make a single significant gift to a DAF. This allows them to capture the full deduction in a high-income year while retaining flexibility to distribute grants to charities over time.

Charitable Bunching

Building on the concept above, charitable bunching focuses on the timing of charitable gifts to maximize their tax efficiency. Each year, taxpayers can either take the standard deduction or itemize expenses. In terms of charitable giving, contributions are deducted from income through an itemized expense report, and the standard deduction acts as a “hurdle” rate.

Most taxpayers do not itemize, but those who do primarily deduct state and local taxes (SALT), mortgage interest, and charitable gifts. Charitable bunching allows donors to consolidate multiple years of donations into a single tax year, enabling them to exceed the standard deduction threshold and capture a greater immediate tax benefit.

While this strategy has been effective for several years, the landscape has changed with the passage of the One Big Beautiful Bill Act (OBBBA) in July 2025. There are three reasons to consider bunching your charitable gifts in 2025 and beyond:

Effective in 2025:

1. SALT (State and Local Tax) Deduction – Increased Cap + Phaseout

Since the passage of the OBBBA, the $10,000 cap on SALT deductions has increased to $40,000 for married filing joint households with Modified Adjusted Gross Income (MAGI) less than $500,000 per year. It begins to phase back down to $10,000 with MAGI between $500,000 and $600,000. For those earning above $600,000, the SALT cap returns to $10,000. Charitable bunching in 2025 can be especially valuable for those above the $600,000 threshold, as illustrated in Scenarios 2 and 3 below. Any level of giving can be beneficial for those with MAGI less than $500,000 and a high level of SALT, as illustrated in Scenario 4 below.

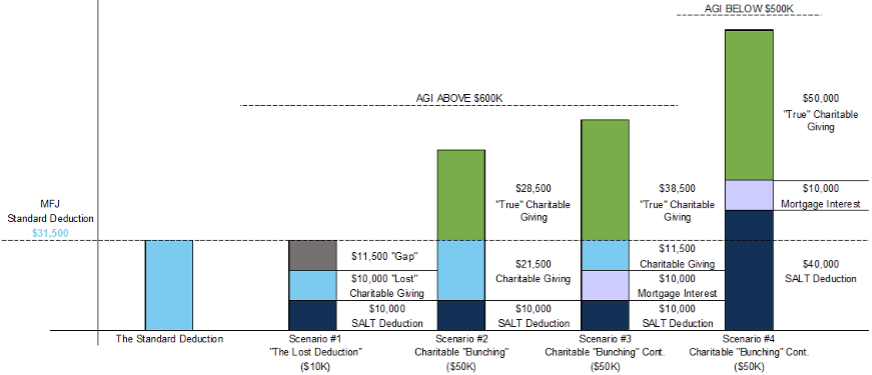

Please refer to the following illustration and scenarios for further explanation:

Scenario #1 – If your aggregate itemized deductions fall below your corresponding standard deduction amount, you should take the standard deduction. As a result, your charitable gift will not receive a tax deduction.

Scenario #2 – To reduce the risk of “lost” deductions if your MAGI is above $600,000, consider the timing of your gifts. For example, if you typically give $10,000 per year, you could give $50,000 this year to fund your giving for the next five years. This strategy is referred to as “charitable bunching.” As a result, you exceed the standard deduction “hurdle rate” and deduct your itemized expenses in the year you chose to “bunch” your gifts.

Scenario #3 – As you incorporate more itemized deductions if your MAGI is above $600,000, your “charitable bunching” offers a more significant tax benefit. Combining charitable giving, SALT, and mortgage interest significantly increases total deductions, pushing them well above the standard deduction and maximizing the tax benefit in the year you bunch your gifts.

Scenario #4 – When combined with mortgage interest and “bunched” charitable giving, total itemized deductions well surpass the standard deduction. This expanded SALT limit allows you to capture an even greater tax benefit in the year you choose to bunch your charitable gifts. In this scenario, we assume the couple’s AGI does not exceed $500,000; thus, they are not subject to the SALT phaseout.

Effective in 2026

2. New floor on deductions for itemizers

Starting in 2026, taxpayers who itemize will only be able to deduct charitable gifts that go beyond 0.5% of their adjusted gross income (AGI). This means a small portion of charitable giving will no longer be deductible under the new rules. For example, a married couple with an AGI of $1M who donates $100,000 would see $5,000 of that donation excluded from their deduction due to the new floor, 0.5% of their AGI.

3. New limits on itemized deductions for top earners: Taxpayers in the top 37% marginal bracket will see their itemized charitable deductions effectively capped at 35% of the deduction’s value.

With the increased SALT limits and pending limitations regarding the deductibility of charitable giving, donors in higher tax brackets might want to consider accelerating their gifts into 2025. Combining charitable bunching with other itemized deductions, such as SALT and mortgage interest, can help ensure you maximize the tax benefit while supporting your philanthropic goals.

Before you consider making larger charitable gifts, please note that your AGI limits charitable deductions. Deductions for charitable cash contributions are limited to 50% or 60% of AGI (depending on whether you give capital gain property in addition to the cash). So, if your AGI is $100,000, you could deduct up to $50,000 or $60,000. Long-term appreciated assets (such as stock held for more than a year) to most charities and donor-advised funds are eligible for a deduction of up to 30% of AGI. If you exceed these limits, you may carry forward the unused portion of your deduction for up to five years. We recommend consulting your CPA and financial advisor about the amount and timing of your charitable gifts.

Qualified Charitable Distributions (QCDS)

This strategy can be effective if you are age 70½ or older. To complete a QCD, you may send up to $108,000 from your IRA directly to a charity each year. The QCD will count towards your required minimum distribution (RMD), if applicable, but will not count towards your taxable income. With lower taxable income and thus lower adjusted gross income (AGI), you may qualify for tax credits/deductions and reduce Medicare IRMAA, amongst other benefits.

One thing to keep in mind if you choose to implement this strategy: QCDs must be completed before taking the remainder of your RMD. Once an RMD has been satisfied, a subsequent QCD cannot retroactively count toward it. Consider prioritizing QCDs earlier in the year before satisfying your remaining RMD.

If you implement this strategy, we recommend working with your CPA and financial advisor to help you follow the IRS rules and navigate tax nuances. For instance, IRA distributions become ineligible for QCD treatment if the funds come directly to you or if they do not end up with a qualified charity.

Of course, we believe it is always important to start by asking why. The “why” for most charitable contributions is not simply to gain a tax deduction but to give back to the communities and people you care about.

Do you or someone you know need help planning your charitable giving activities? Contact the SignatureGENEROSITY team at SignatureGENEROSITY@signaturefd.com to learn more about our approach to strategic generosity and start your personalized Generosity Blueprint journey.